Latest Articles

View our recent updates.

Strategic Project Summary

Over the past year, I deployed capital and research effort into two major strategic finance and technology initiatives focused on the future of systematic investing, liquidity infrastructure, and automated execution systems.

Project 1 — Blockchain Liquidity Infrastructure...

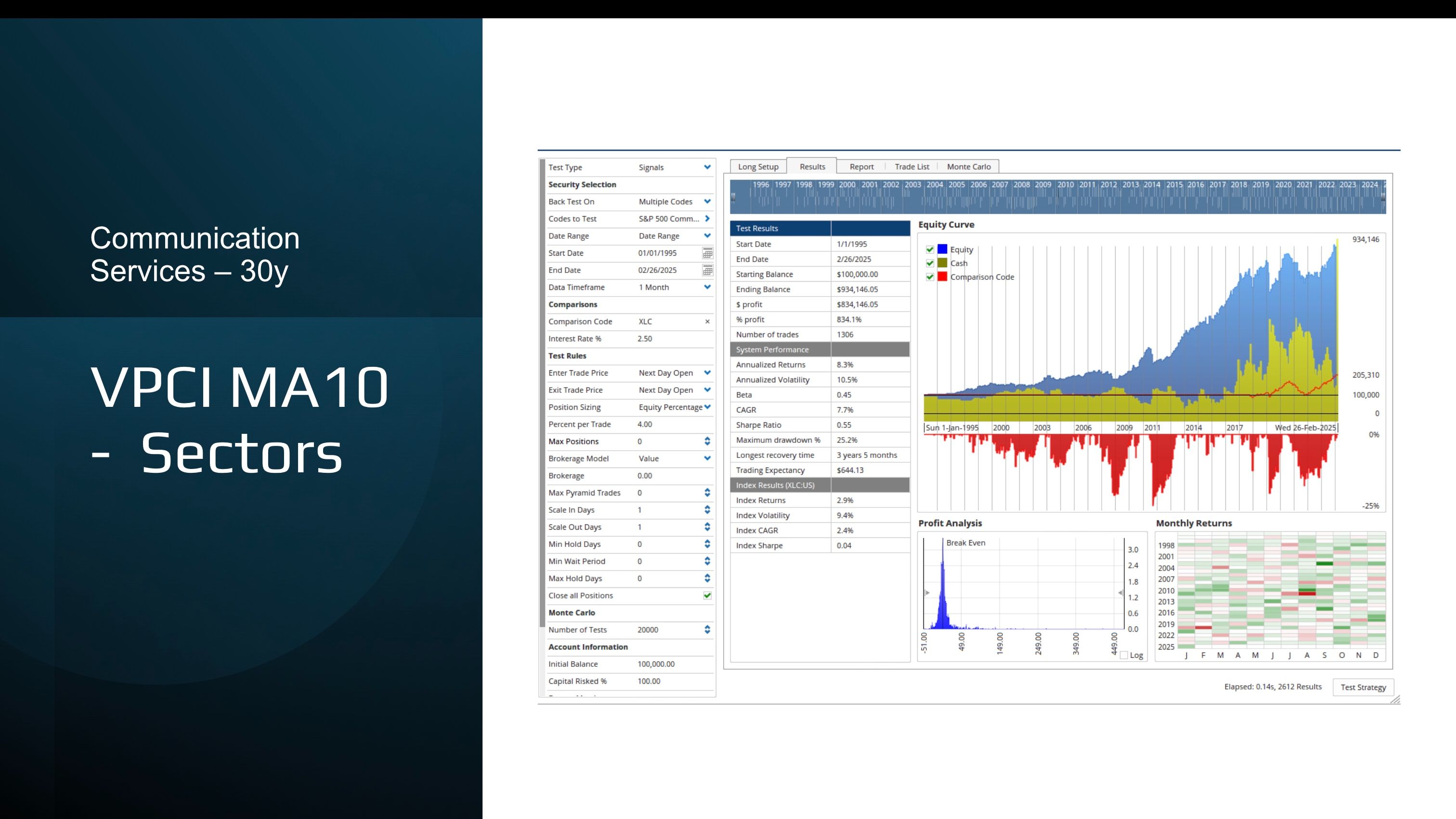

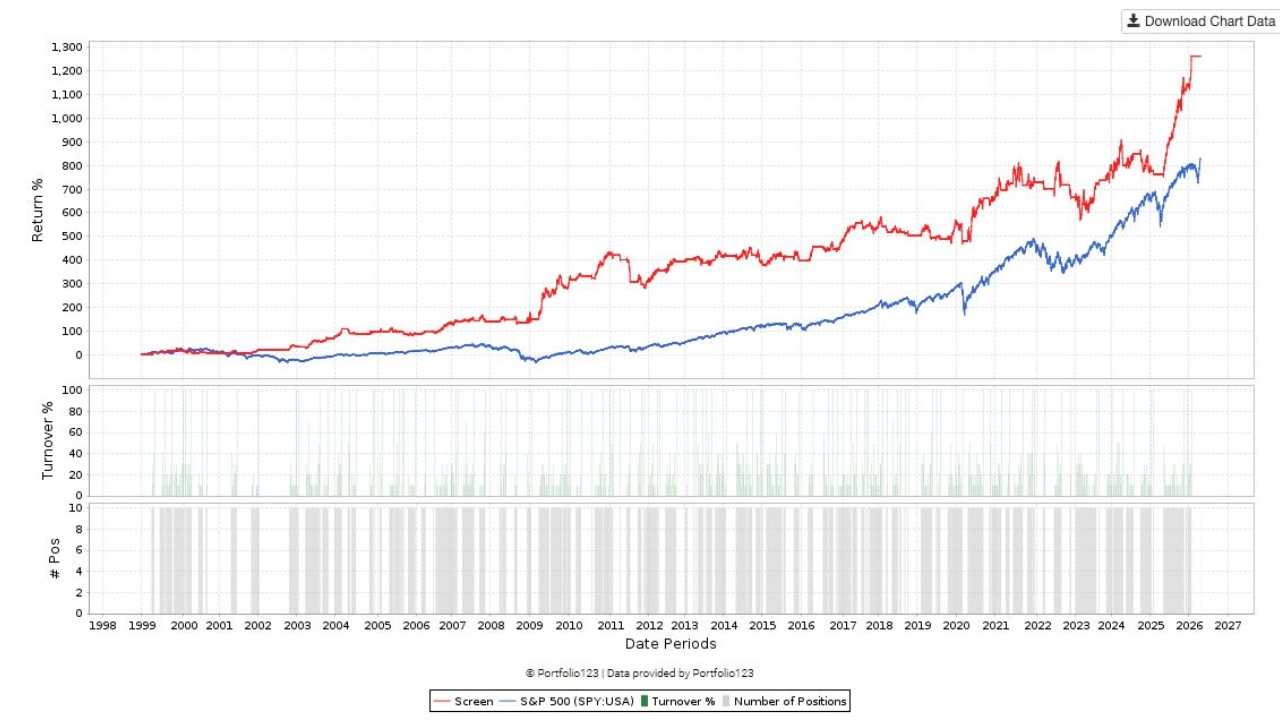

Volume Price Confirmation Indicator (VPCI) MA10 Tactical Sector Rotation Model

The VPCI MA10 Tactical Model combines the Volume Price Confirmation Indicator (VPCI) with a 10-period moving average filter to identify oversold conditions and potential trend reversals across major market sectors.

The ...

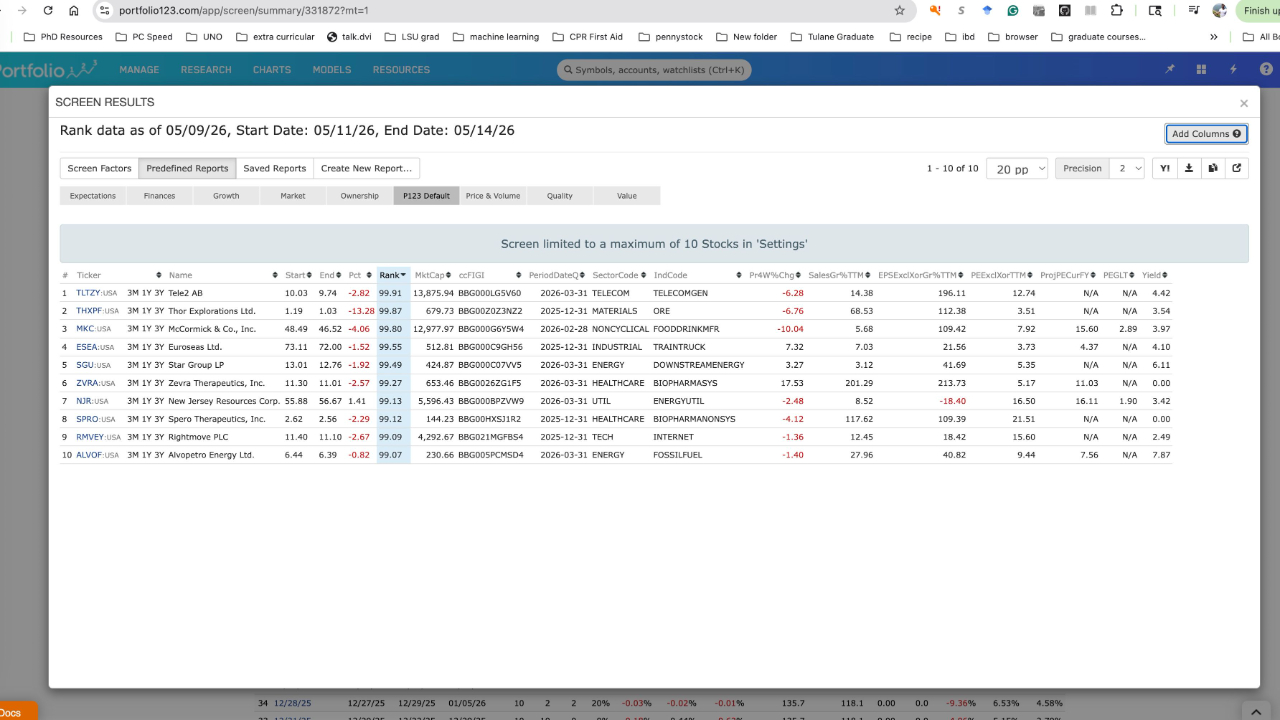

This screen is interesting because the model is clearly surfacing a mix of:

-

Deep value

-

Earnings acceleration

-

High sales growth

-

Low projected valuation multiples

-

High ranking composite factors

The portfolio appears heavily tilted toward:

-

Small/mid cap opportunistic

...

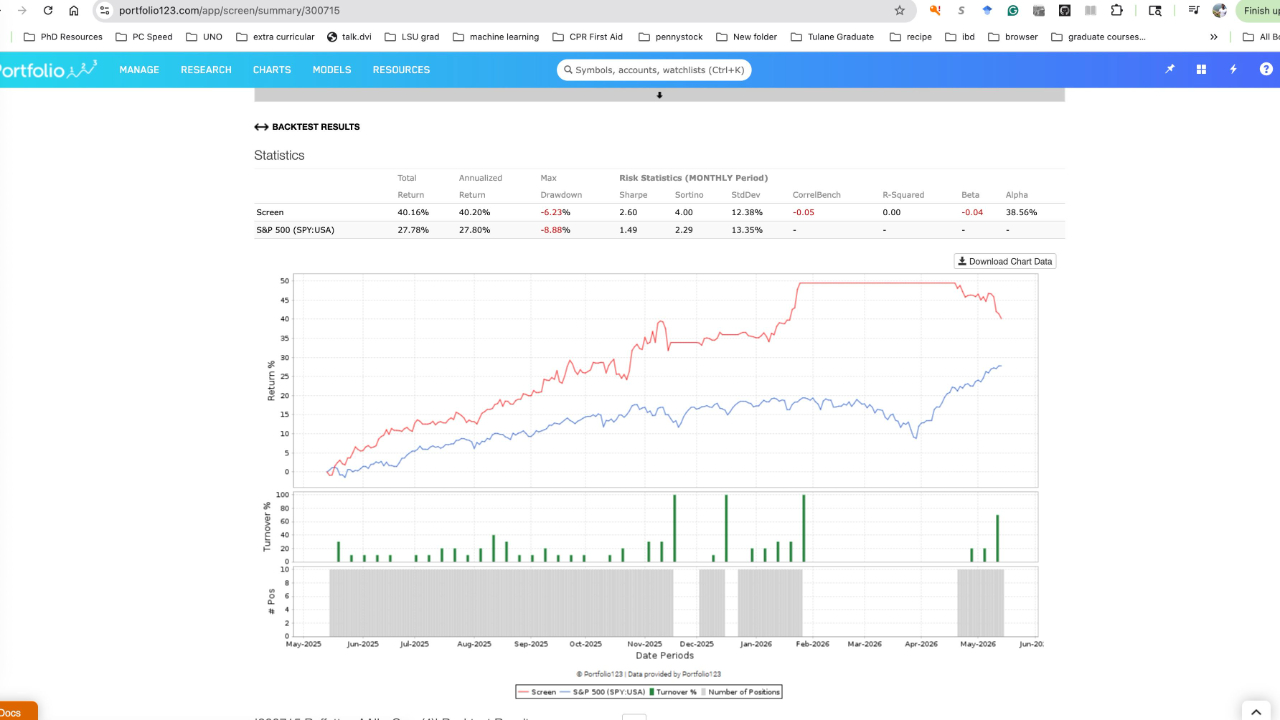

Sharpe & Sortino in Action: A Real-Time Portfolio Focused on Risk-Adjusted Returns

Markets don’t reward investors simply for taking risk. They reward investors for taking efficient risk.

Over the last year, this real-time portfolio model focused on high Sharpe Ratio and Sortino Ratio characteristi...

I’m currently looking for help expanding the marketing reach of my finance education and portfolio platform.

Compensation ranges from 30%–70% revenue share depending on the product, structure, and level of involvement. The role would involve leveraging your own network, paid advertising strateg...

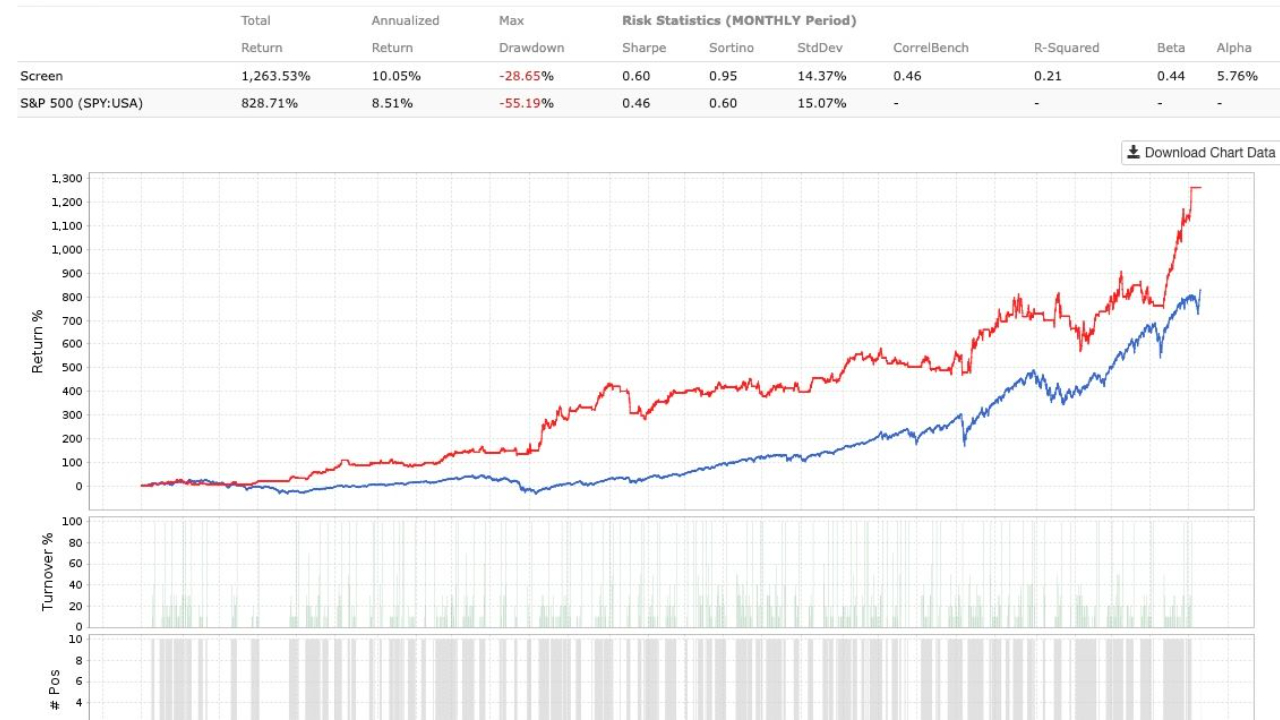

Tactical Re-Entry: How the Portfolio Transitioned Back Into the Market

One of the most important aspects of tactical investing is understanding that market exposure is not static.

The goal is not to remain permanently bullish or permanently defensive.

Instead, the objective is to adapt exposure a...