Lutey Moderate Growth - Simplified CAN SLIM

Core Philosophy

Buy companies with accelerating earnings whose stock prices are already confirming that strength by trading near new highs.

This aligns with the original CAN SLIM insight:

-

Fundamentals lead

-

Price confirms

-

You enter before institutional ownership becomes crowded

Simplified CAN SLIM (ACS) Screening Rules

The ACS model uses only two objective filters:

1. Earnings Growth Filter (Fundamental Strength)

A stock must show both long-term consistency and short-term acceleration:

-

≥ 15% average annual EPS growth over the past 5 years

-

≥ 25% EPS growth in the most recent quarter

(compared to the same quarter one year earlier)

This ensures you are buying:

-

Proven growers (not one-off stories)

-

Companies with recent earnings acceleration

2. Price Confirmation Filter (Momentum Validation)

-

Current stock price is within 10% of its all-time high

This avoids:

-

Value traps

-

Turnaround speculation

-

Stocks rising only on hope rather than demand

Price near highs confirms institutional accumulation and demand dominance.

Step-by-Step Implementation Guide

Step 1: Define Your Universe

-

Use liquid, exchange-listed stocks (NYSE / NASDAQ)

-

Avoid micro-caps and illiquid names

Step 2: Run the Earnings Screen

Filter stocks that meet both:

-

5-year average EPS growth ≥ 15%

-

Most recent quarterly EPS growth ≥ 25% YoY

This can be done using:

-

FactSet, Portfolio123, Bloomberg, or similar data sources

-

A simple Python or spreadsheet screen if data is available

Step 3: Apply the Price Filter

From the earnings-qualified list, keep only stocks where:

-

Current price ≥ 90% of the stock’s all-time high

This ensures trend confirmation, not prediction.

Step 4: Portfolio Construction

-

Hold all passing stocks (no discretionary selection)

-

Equal-weight positions

-

Avoid over-concentration in one sector

Step 5: Rebalancing

-

Rebalance monthly

-

Remove stocks that no longer meet the criteria

-

Add new stocks that pass the screen

This maintains exposure to current leadership, not legacy winners.

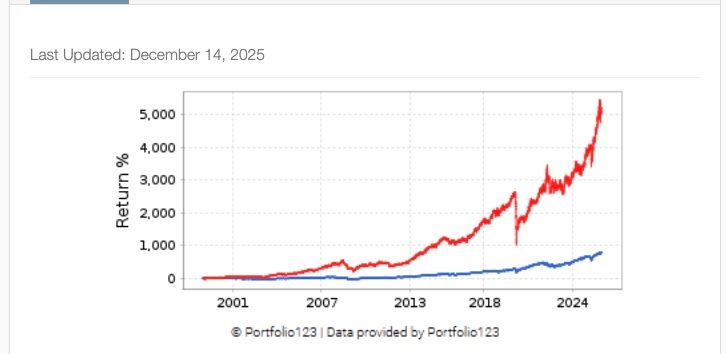

Invest in the Lutey Moderate Growth PortfolioLutey Moderate Growth: Simplified CAN SLIM All U.S. Stock (Nyse/Nasdaq) components.

268% Total Returns

15.4% Annualized

Beta ~0.89 | -118% Downside Capture

Growth with Defense.

Downside Protection.

Compounding Capital.

Superior drawdown control—core holding for risk-aware advisors and clients.

ACS Model — Lower Volatility Growth with Defensive Tilt

Return Profile

Total Return: 268.5%

Annualized Return (10-yr): 15.4%

Alpha: +5.7% to +9.1%

Upside Capture: 299%

Downside Capture: -118% (meaning downside reduction vs market)

Risk Profile

Volatility: 22.9%

Beta: ~0.89

Sharpe Ratio: 0.60

Sortino Ratio: 0.66

Interpretation

Designed to capture upside while actively limiting downside risk.

Provides significant drawdown protection.

Best risk-controlled growth strategy.

Best Use Case

Core allocation for risk-aware investors.

Strong fit for advisory portfolios, tactical allocations, and conservative growth mandates.

A real time $400,000 case study

The Lutey Moderate Growth 'Simplified CAN SLIM' portfolio applied to the SP500 components in real time February 2025. The passing stocks were held with a model $400,000 portfolio in portfolio123.com as a live forward tested study.

The performance of the model is 28.17% over the past 12 months (as of Jan 2026). The red line in the image below represents the growth of the portfolio from the initial rebalance in February 2025 during the last 12 months.

Lutey Moderate Growth - Simplified CAN SLIM: SP500 Components.

490% Returns with 50–60% of the Market Risk

490% Cumulative Returns

Beta ~0.50–0.60

7–16% Alpha Every Horizon

Simplified Growth.

Controlled Risk.

Compounding Capital.

2.5x S&P 500 with half the beta—rules-based CAN SLIM for advisors and clients.

Simplified CAN SLIM Model: High-Conviction Growth with Systematic Risk Control

The Simplified CAN SLIM Model is designed to capture equity growth through a focused, rules-based selection process, emphasizing only the most persistent drivers of long-term outperformance. By stripping CAN SLIM down to its most effective components, the model aims to maximize alpha while maintaining disciplined market exposure.

From 7/1/2013 through 6/30/2023, the strategy delivered exceptional long-term performance, materially outperforming the S&P 500 and a blended benchmark across every evaluated horizon.

Key highlights:

-

Powerful long-term compounding: The model generated nearly 490% cumulative returns, more than 2.5× the S&P 500 over the same period.

-

Strong and persistent alpha: Alpha remained positive across all timeframes, ranging from approximately 7% to over 16%, driven by stock selection rather than market beta.

-

Lower market dependence: Beta remained near 0.50–0.60, significantly reducing reliance on broad market movements.

-

Efficient volatility profile: Standard deviation was slightly below the S&P 500, despite meaningfully higher returns.

-

Superior risk-adjusted performance: Sharpe and Sortino ratios exceeded the S&P 500 across intermediate and long-term horizons, indicating efficient use of risk.

-

Disciplined participation: The model maintained consistent upside participation while applying systematic rules to manage downside exposure.

The Simplified CAN SLIM Model uses a quantitative, repeatable framework focused on earnings strength, price momentum, and market confirmation, while eliminating discretionary decisions. The result is a strategy that is easy to implement, scalable across accounts, and intuitive for clients to understand.

For advisors, this model can serve as:

-

A core growth allocation within diversified portfolios

-

A high-alpha satellite sleeve complementing lower-volatility strategies

-

A transparent, rules-based approach aligned with modern portfolio construction

For clients, the promise is straightforward:

A focused growth strategy built to compound capital efficiently over full market cycles.

A case study: Lutey Moderate Growth 'Simplified CAN SLIM' with tactical risk overlay

This model achieves high returns while providing the benefit of reduced risk. Lower standard deviation than the SP500 historically with weekly updates to the passing stocks and risk overlay. Achieves higher return than the overall market historically and overlapping sub periods.

Lutey Moderate Growth: Simplified CAN SLIM All U.S. Stock (Nyse/Nasdaq) components.

w/ Weekly Risk Overlay

146% Total Returns

Beta ~0.24

13.3% Volatility (Lowest Growth)

Balanced Growth.

Ultra-Smooth Ride.

Compounding Capital.

9.8% annualized with top risk-adjusted profile—core for advisors and clients

Lutey Moderate Growth – ACS (Tactical)

Balanced Risk-Managed Growth

Return Profile

Total Return: 146.3%

Annualized Return (10-yr): ~9.8%

Alpha: +3.1% to +5.6%

Upside Capture: ~-46%

Downside Capture: ~-29%

Risk Profile

Beta: ~0.24

Volatility: 13.3% (lowest of all growth models)

Sharpe Ratio: 0.61

Sortino Ratio: 0.70

Interpretation

One of the best risk-adjusted tactical profiles.

Meaningfully smoother equity curve than all-stock ACS.

Strong balance between growth participation and capital protection.

Best Use Case

Core holding for risk-aware investors.

Excellent fit for advisor model portfolios and retirement accounts.