Portfolio Mastery Portfolio Mastery

Learning outcomes:

Learn to master the investment philosophy of 60% equity - 40% debt and auto tactical allocation between debt and equity based on the business cycle and market environment. A 25 hour coaching - webinar / video series. Updated to current economic and market conditions with two implementation courses.

Lessons 1–12 are designed to help you build and implement the full portfolio system from the ground up.

In Lessons 1–5, you will get set up inside Portfolio123, rebuild the stock screens, set up your brokerage account, and learn how to automate copy trading so you can begin following the models in your own account. Each of these early lessons includes a live one-on-one follow-up to make sure your setup is working correctly and that you understand how to apply it.

From there, the program shifts into the bigger picture: understanding the macroeconomic environment, identifying the most important leading indicators, and learning how to combine those signals with the portfolio’s passing stocks to create an optimal investment framework for all economic conditions.

If you want, I can turn this into:

1. a premium program description,

2. a Kajabi sales page section,

3. or a webinar pitch version.

The second half of the program is where everything becomes actionable.

In the final 5 lessons, you’ll learn the exact trading rules I use to identify which stocks are most likely to move — before they move.

We break this down across multiple time horizons:

• 1–2 day momentum setups

• 1–2 week swing opportunities

• 3–4 week trend positioning

You’ll learn how to read price, volume, and structure together to determine:

• Which stocks are most likely to go up

• Which stocks are most likely to go down

• When to enter, when to exit, and when to stay out

This is a complete technical framework — not theory — built around real setups that can be applied immediately alongside the portfolio models.

We focus on:

• Identifying high-probability moves early

• Avoiding low-quality trades

• Executing with precision and discipline

The program concludes with a final one-on-one wrap-up call where we refine your system, answer questions, and make sure you’re fully confident applying everything. Plus one additional bonus call to cover whatever you want. After the implementation call is over.

The specific learning outcomes for the first half of the program are below:

Learn to build and follow both growth and defensive investing strategies to build the optimal portfolio framework shown in the image at the bottom of the page. Plus learn the exact mindset needed to adjust your portfolio and settings and adapt to the current market environment on your own. After the mastery program is done. Regardless of prior finance background.

1. Expansion (Full Growth Mode)

80/20 Equity/Bonds

CAN SLIM + Graham

Momentum leaders + value screens

Max upside capture (215% market)

LRI Signals: Normal yield curve + bullish volume

2. Late Cycle Warning (Tactical Shift)

70/30 Equity/Bonds -> 60/40 Equity/Bonds

Risk Overlay Activates

Momentum rules dial back exposure

Tactical risk overlay + value tilt for protection

LRI: Yield inversion + slowing breadth

3. Confirmed Sell-Off (Risk OFF)

50/50 Equity/Bonds

Buffet Lutey Value + Tactical Overlay

Defensive value screens

Momentum filters kill losers

Capital preservation priority

LRI: Death cross + volume failure

4. Early Recovery (Value Ramp)

60/40 -> 70/30 → Gradual Re-Entry

Buffet Lutey Value + Tactical Overlay

Mean reversion winners

Tactical momentum confirms base

LRI: Inversion unwinds

5. New Cycle (Back to Growth)

80/20 Full Offensive

Growth CAN SLIM Momentum Returns

Leadership rotation

Growth screens dominate

LRI: All signals green

Apply principles and best practices from my recent research. To achieve optimal portfolio allocations.

Learn to stride between 60% equity and 40% debt based on your own comfort level. Lern what stocks to hold and own based on the current phase of the market.

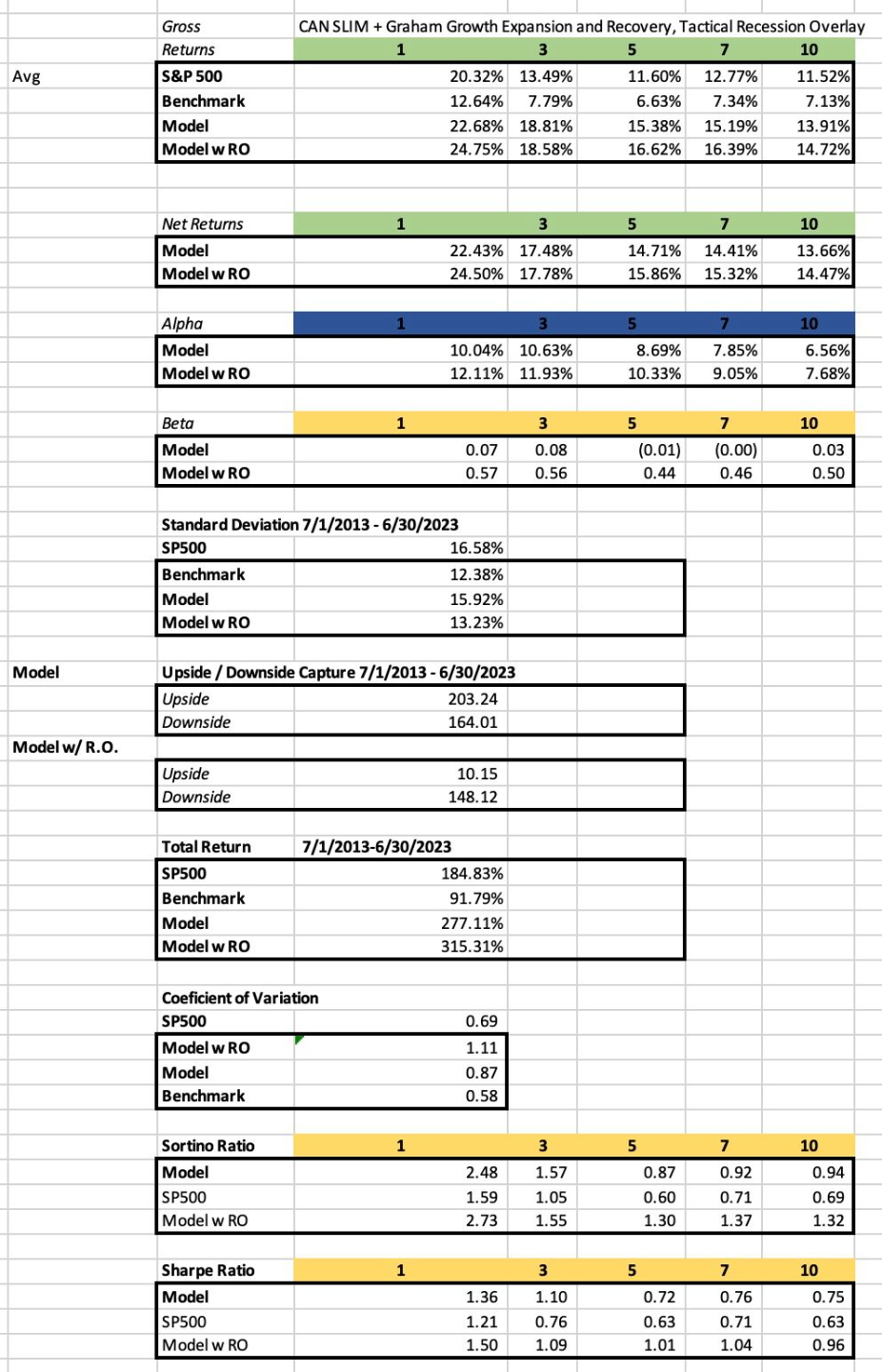

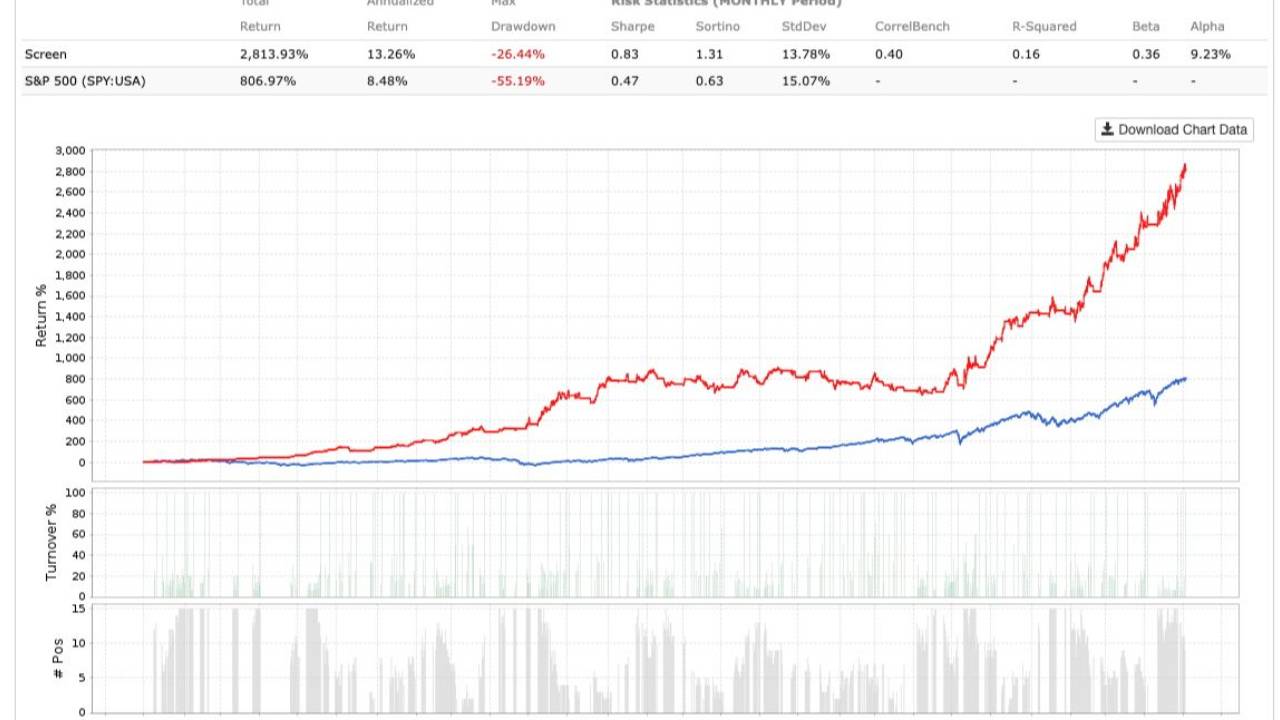

Learn the portfolio rules and strategies used to build a efficient portfolio with lower standard deviation than the overall market (SP500) - with higher Sortino and higher Sharpe Ratios and a less severe maximum drawdown.

Learn the model shown in the images above👆🏼

Learn to re-build and receive a copy of the complete portfolio tracking spreadsheet. Learn to utilize concepts like Sortino Ratio, upside and downside capture to understand risk and performance- while tracking the portfolio over a longer time-horizon while capturing a point-in time snapshot to validate the results. Rebuild the exact system you want to use together with my guidance. - A complete system overhaul.

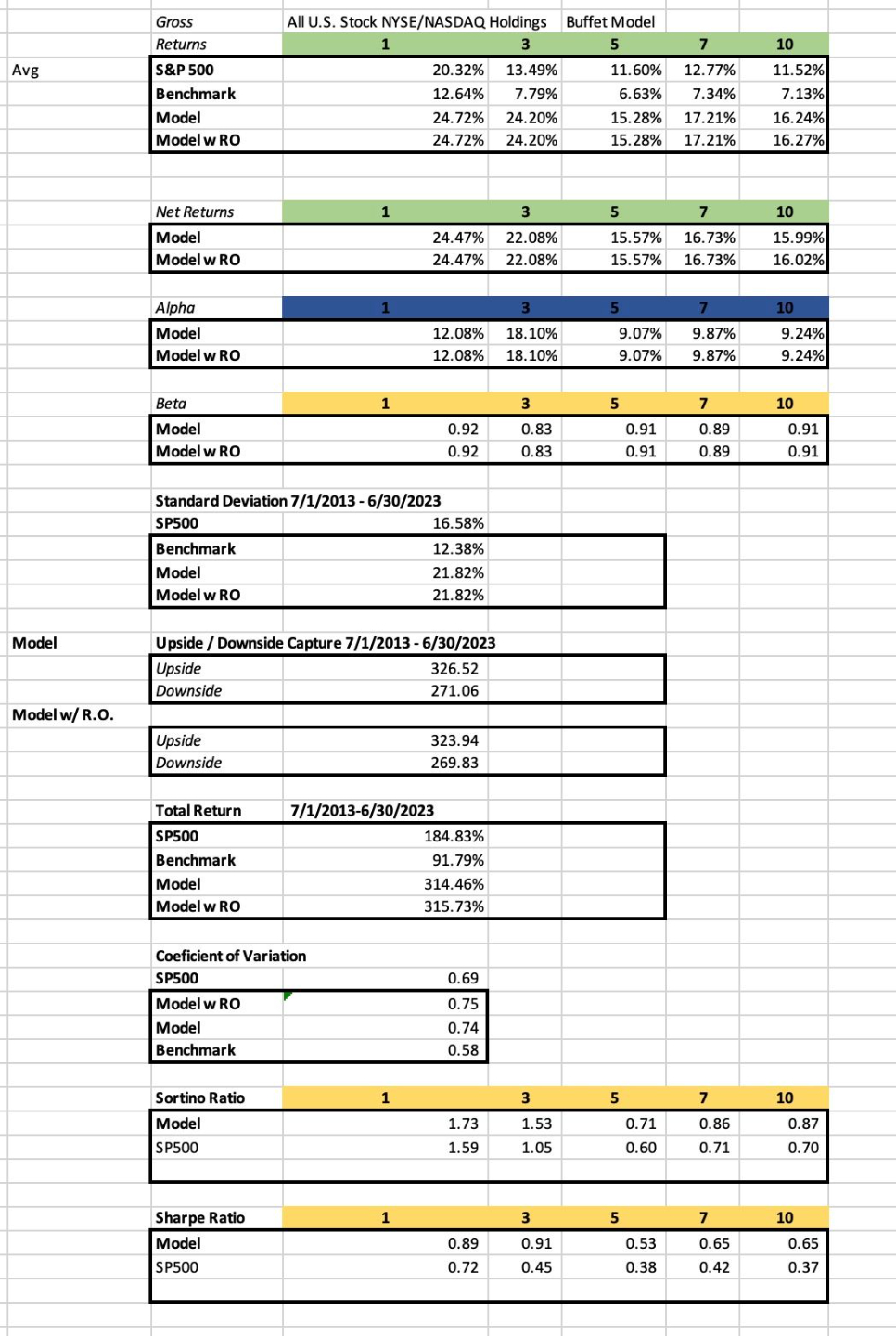

Learn to improve your returns while lowering the standard deviation. Seen in the image 👇🏼below - which shows roughly the same return and with a higher standard deviation - thus no tactical risk preservation benefit.

The result is improved by applying the tactical risk overlay principles and defensive switching practice following the 2025 (Journal of International Finance and Economics - JIFE) Lutey Recession Rule.

The current framework represents the most up-to-date evolution of this research

It combines optimal portfolio construction with tactical regime switching:

-

60% equity / 40% debt during market turning points

-

80% equity / 20% debt during confirmed growth periods

Over the past decade, this tactical approach has outperformed the S&P 500 by:

-

+4% average annual return (1-year)

-

+11% (3-year average)

-

+4% (5-year average)

-

+4% (7-year average)

-

+5% (10-year average)

At the same time, portfolio standard deviation has been reduced by approximately 3% compared to following the strategy without the tactical switching component of the Lutey Recession Indicator.

Invest in the Framework — Not Just the Education

Gain access to the models that drive institutional-level investment decisions without needing a graduate degree in quantitative finance to build them yourself.

Inside the program, you will:

-

Learn the portfolio architecture that drives the returns

-

Build your own implementation spreadsheet

-

Compare your work against a complete reference model

-

Develop your own allocation philosophy

You will ultimately determine your preferred positioning:

-

Aggressive growth (higher risk / higher return)

-

Blended growth and value

-

Passive core with tactical overlays

-

Fully tactical hybrid designed to preserve capital during market turning points and re-engage during recovery phases

Ongoing Model Access

For those who want continued portfolio updates beyond the video training and 1-on-1 implementation sessions, an additional 0.25% management fee provides:

-

Ongoing portfolio recommendations

-

Tactical updates

-

Allocation guidance

-

Research enhancements throughout the year

Who This Is For

Whether you are:

-

An individual investor seeking to manage capital independently alongside an experienced professional — without the overhead of a traditional financial planning firm

-

Or a financial planner looking to integrate research-backed portfolio frameworks into your client offerings

You can subscribe to a customized combination of products tailored to your investing experience and objectives.

Follow the prompts in the cart to build the mix that aligns with your goals — and take structured control of your financial future.

Learn the most in depth portfolio information in this course - start where you are and work together to build your tactical portfolio. Take the advice I lay out or steer the conversation in your own direction.

I'm here for you and your success.

Invest now!