Simplified CAN SLIM Weekly Portfolio

Weekly portfolio recommendations following the simplified CAN SLIM model with capital weighted volume risk overlay.

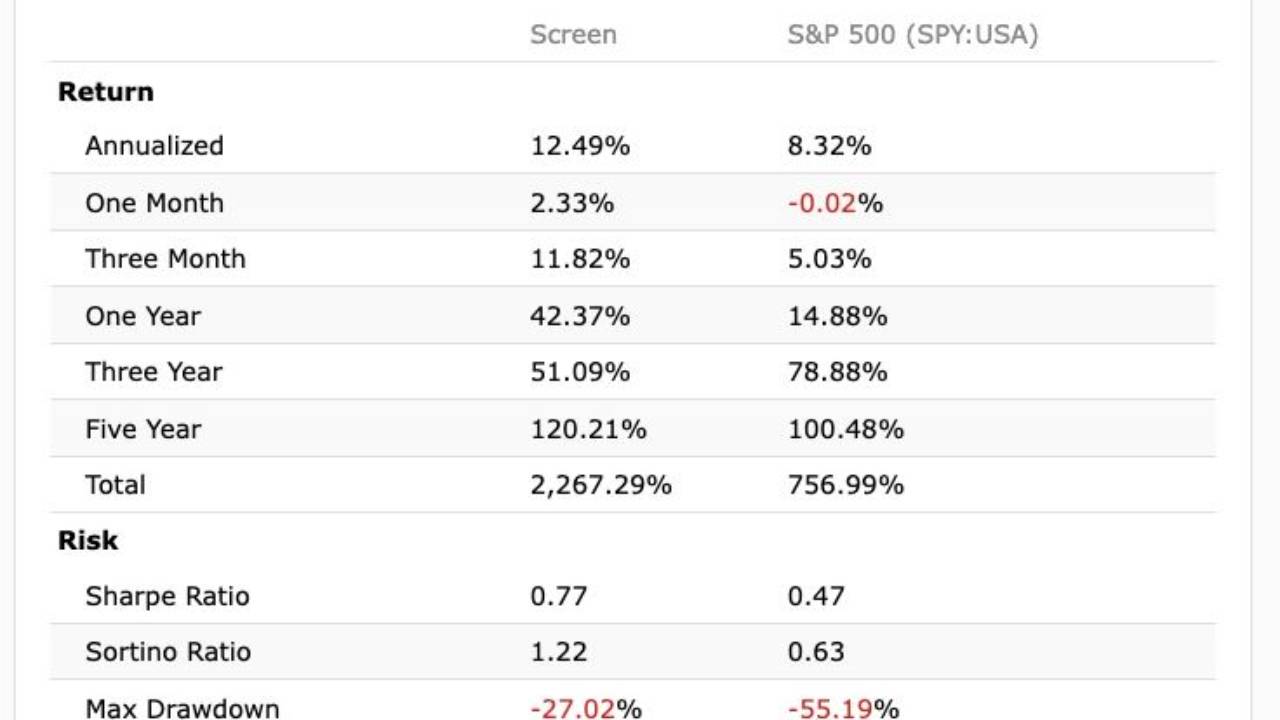

As published in the Journal of Investing 2025. A compliment to the CAN SLIM model and other Famous Investor Models with Growth properties. The model historically outperforms on return and underperforms on risk. Historical performance is a good measure of expected future performance.

Weekly portfolio recommendations following the Lutey Moderate Growth 'Simplified CANSLIM' Investing Strategy. Capital Weighted Volume risk overlay added. Higher return and lower risk than the SP500.

These portfolios apply the risk-return properties of Capital Weighted Volume - Famous Investor Portfolios - Lutey (2025 - Journal of Investing). They drastically reduce the portfolio standard deviation while improving both the Sharpe and Sortino ratios and improving the maximum drawdown. While preserving the portfolio return.

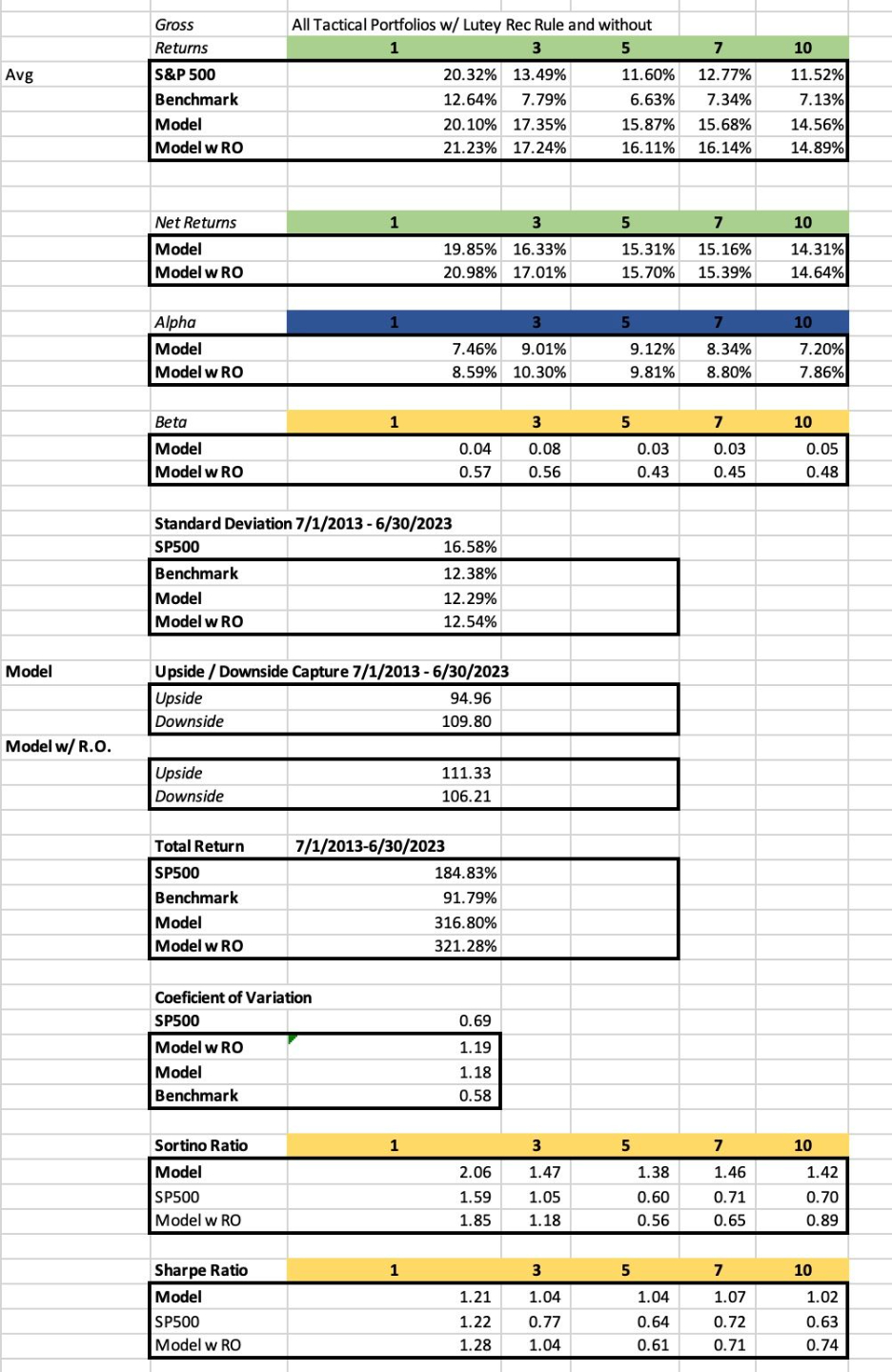

They are stand-alone portfolios that may be combined and used in a system for portfolio management with the other stand alone monthly portfolios - or other weekly tactical portfolios. A case study that explores investment across all tactical risk-overlay portfolios is shown below. The other portfolios are available on request or at check out.

See the CAN SLIM portfolio with risk overlay

Let the Weekly Tactical Risk Overlay Make the Hard Decisions for You.

Stop guessing when to go aggressive and when to pull back.

Our research-backed Weekly Tactical Risk Overlay tells you when to lean into opportunity — and when to reduce exposure — guiding your active vs. passive allocation decisions week by week.

Inside the framework:

-

🔁 Actively rotate into leading sectors using the Lutey Growth / CAN SLIM methodology

-

🛡 Apply a disciplined weekly risk overlay to manage drawdowns and market regime shifts

-

📊 Follow a rules-based process grounded in peer-reviewed academic research

This strategy is supported by published research in:

-

Journal of International Finance and Economics (JIFE, 2024)

-

Applied Finance Letters (AFL, 2023)

-

Journal of Investing (JOI, 2025) — introducing the weekly tactical risk overlay framework

The result?

A structured system that combines:

-

Growth investing during expansion phases

-

Tactical defense during market stress

-

Evidence-based allocation shifts — not emotional reactions

Move from reactive investing to systematic decision-making.

Build, rotate, defend, and re-deploy capital with a research-backed edge.