Lutey Growth - Benjamin Graham Investing Portfolio

Graham Investing Style — Summary

-

Emphasis on capital preservation

-

Preference for financial strength over growth

-

Focus on cheap, stable, dividend-paying firms

-

Avoidance of speculation, leverage, and distress risk

In contrast to CAN SLIM, Graham explicitly prioritizes valuation and balance-sheet safety, not momentum or innovation

Stock Selection Rules (Operational Graham Screen)

The paper operationalizes Graham’s ideas into objective, replicable screening rules (Appendix I). A stock must satisfy all of the following:

1. Liquidity & Tradability Filter

- Exclude OTC stocks

- Ensures sufficient liquidity and data quality

2. Balance Sheet Strength

- Current Ratio ≥ 1.5

- (Current Assets / Current Liabilities)

- Ensures short-term solvency and working-capital cushion

- Long-term debt ≤ 110% of working capital

- (LT Debt ≤ 1.1 × (Current Assets − Current Liabilities))

- Explicit leverage constraint consistent with Graham’s defensive criteria

3. Earnings Stability (Key Graham Requirement)

- Positive EPS in each of the last four quarters

- Positive EPS in each of the last five years

This rule avoids:

Speculative cyclicals

Firms dependent on macro timing

4. Earnings Growth (Conservative, Not Aggressive)

- EPS this year > EPS last year

- EPS this year > EPS five years ago

- Ensures slow, sustainable growth rather than acceleration

5. Dividend Requirement

- Firm must have paid a dividend in the past year

- Acts as a quality and discipline signal

- Aligns with Graham’s preference for shareholder return and cash-flow reliability

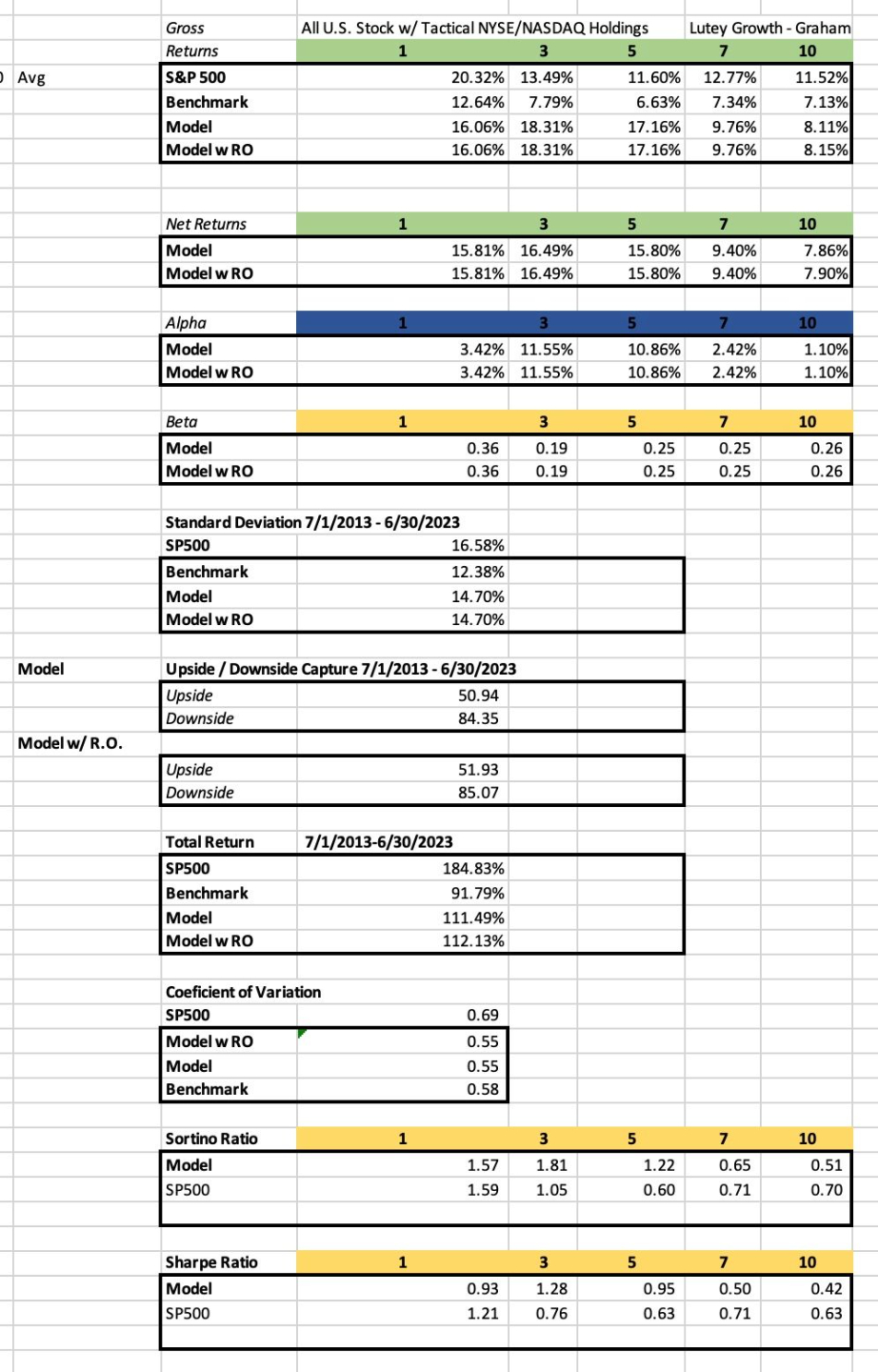

Lutey Growth: Graham - All Stock (NYSE/Nasdaq)

314% Total Returns

16.2% Annualized

Beta ~0.90 | 327% Upside Capture

Ultra-Convex Growth.

Aggressive Alpha.

Compounding Capital.

Massive upside with drawdown discipline—satellite powerhouse for advisors and clients.

Return Profile

Total Return: 314.5%

Annualized Return (10-yr): 16.2%

Alpha: +9.2% to +18.1%

Upside Capture: 327%

Downside Capture: 271%

Risk Profile

Volatility: 21.8%

Beta: ~0.90

Sharpe Ratio: 0.65

Sortino Ratio: 0.87

Interpretation

Ultra-convex factor strategy — captures massive upside but with meaningful drawdowns.

Most aggressive return profile after CAN SLIM.

Produces huge upside beta but also participates heavily in market declines.

Best Use Case

Strong alpha generator inside already efficient portfolios.

Strong complement to defensive or tactical risk overlays.

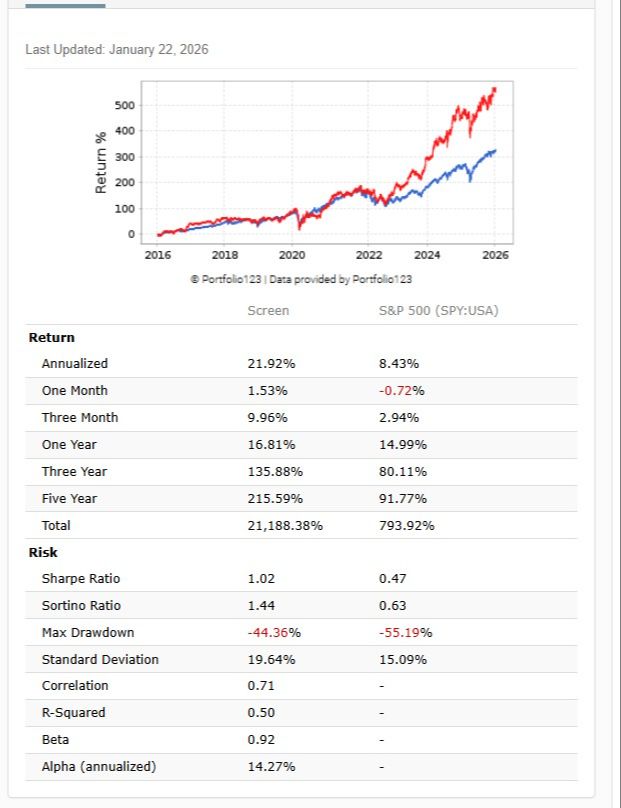

A real time $400,000 case study

The Lutey Growth 'Graham' portfolio applied to the SP500 components in real time February 2025. The passing stocks were held with a model $400,000 portfolio in portfolio123.com as a live forward tested study.

The performance of the model is 33.25% over the past 12 months (as of Jan 2026). The red line in the image below represents the growth of the portfolio from the initial rebalance in February 2025 during the last 12 months.

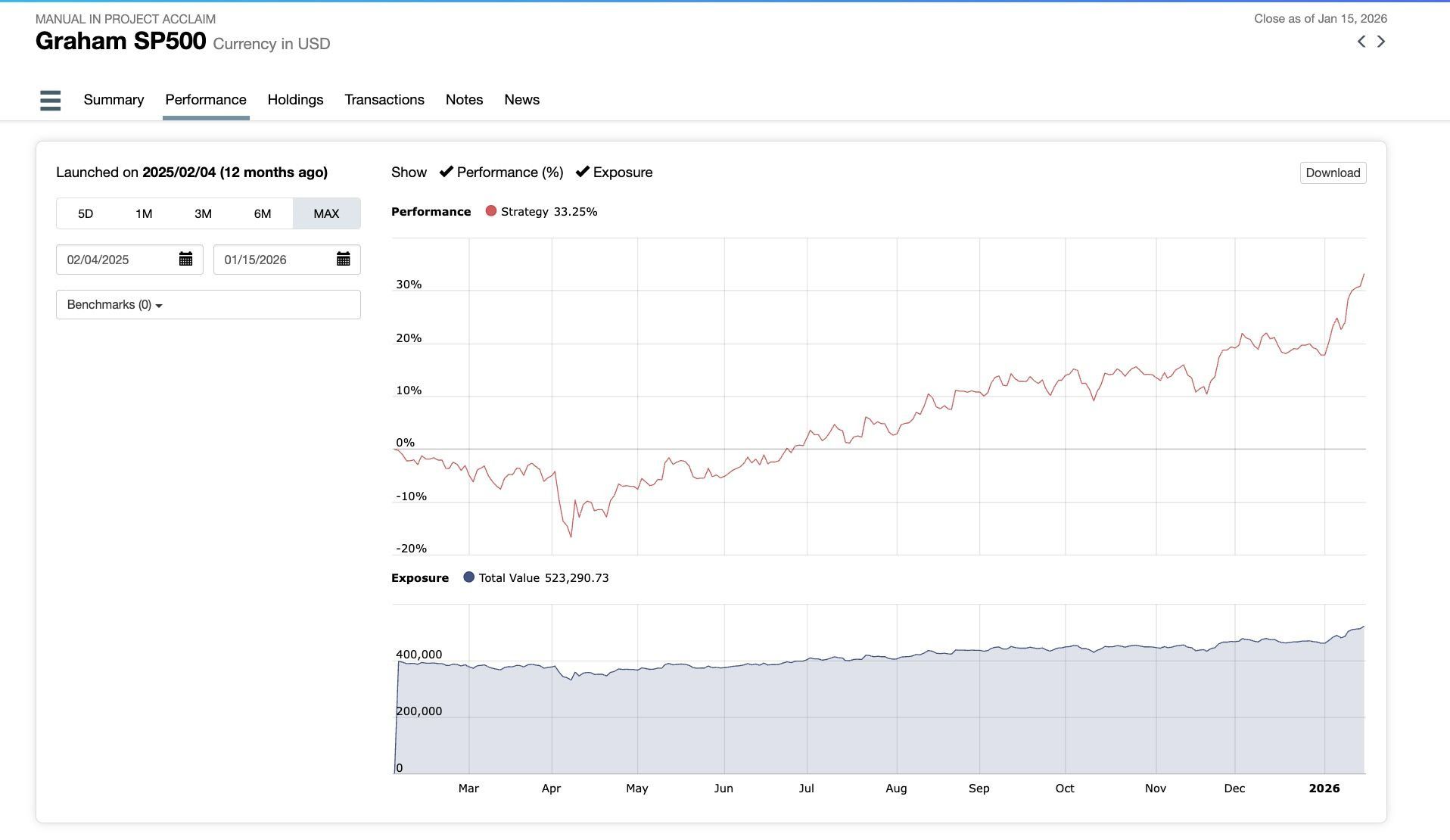

Lutey Growth - Benjamin Graham: SP500 Components.

Relentless Growth.

Unshakable Protection.

420%+ Returns

Beta < 1.0

Alpha in Every Horizon

Equity Upside.

Disciplined Downside.

Compounding Capital.

Outperforms S&P 500 with lower risk—style-agnostic, rules-based growth for advisors and clients.

A Disciplined, Risk-Aware Equity Model Built to Compound Capital

This model is designed for advisors and clients who want equity-like upside with intentional risk management, not benchmark hugging or black-box leverage.

Over a full market cycle (7/1/2013–6/30/2023), the strategy delivered material outperformance versus the S&P 500 and a blended benchmark, while maintaining controlled market exposure (β < 1) and a repeatable, rules-based process.

Why it stands out:

-

Strong long-term compounding: Total returns exceeded 420%, more than double the S&P 500 over the same period.

-

Persistent alpha: Annualized alpha remained positive across 1-, 3-, 5-, 7-, and 10-year horizons.

-

Risk-aware participation: Beta consistently below 1.0, indicating less sensitivity to broad market drawdowns.

-

Superior risk-adjusted returns: Sharpe and Sortino ratios materially exceeded the S&P 500 across all timeframes.

-

Upside capture with discipline: The model participates meaningfully in rising markets while using systematic rules to manage exposure during stress periods.

The strategy is style-agnostic and adaptive, blending growth and value signals with macro-aware allocation logic. It is designed to complement traditional portfolios—either as a core equity holding or a satellite alpha sleeve—without relying on leverage, market timing discretion, or subjective judgment.

For advisors, this means:

-

A transparent, rules-based model you can explain to clients

-

Repeatable implementation across accounts

-

A framework focused on long-term capital growth, not short-term noise

For clients, it means a simple promise:

Participate in market growth, manage downside intelligently, and compound capital over time.

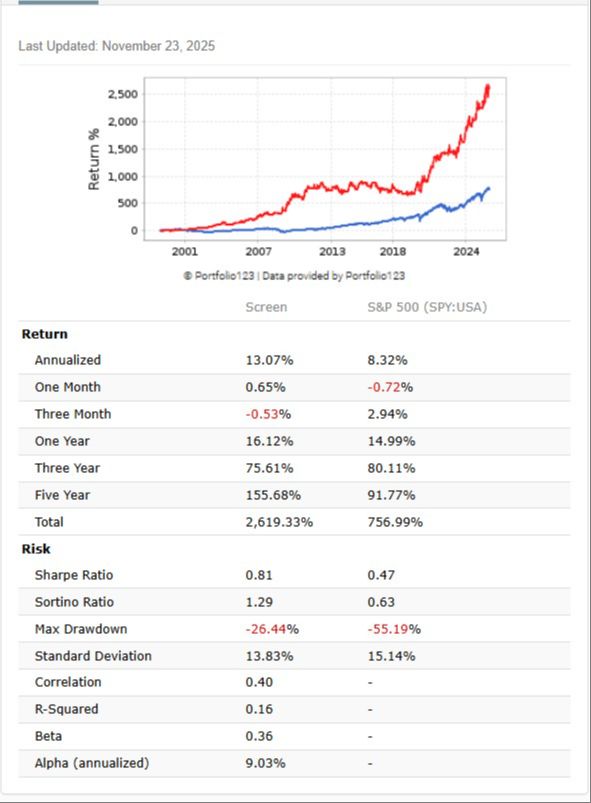

A tactical weekly real time look at the Lutey Growth - Graham

The Lutey Growth 'Graham' model with weekly rebalancing. This significantly cuts the risk out of the portfolio by applying a tactical risk overlay.

This lowers the standard deviation of the portfolio to just over 13% while preserving the high return. It uses the passing stocks each week and decision for whether to be in the market or not to reduce exposure during market downturns and gain an edge during the market upswings.

View the Model

Lutey Growth: Graham - All Stock (NYSE/Nasdaq)

w/ Weekly Risk Overlay

112% Total Returns

Beta ~0.25

Alpha +1–11% Every Horizon

Graham Factor Alpha.

Controlled Exposure.

Compounding Capital.

Steady returns with low volatility—factor diversifier for advisors and clients.

Lutey Growth – Graham (Tactical)

Factor Alpha with Controlled Exposure

Return Profile

Total Return: 111.5%

Annualized Return (10-yr): ~7.9%

Alpha: +1.1% to +10.9%

Upside Capture: ~51%

Downside Capture: ~85%

Risk Profile

Beta: ~0.25

Volatility: 14.7%

Sharpe Ratio: 0.42

Sortino Ratio: 0.51

Coefficient of Variation: 0.55

Interpretation

Tactical overlay neutralizes Graham’s natural convexity.

Lower return than all-stock version, but far less drawdown risk.

Turns Graham into a steady factor exposure rather than a swing-for-the-fences model.

Best Use Case

Factor diversification inside conservative portfolios.

Complement to tactical CAN SLIM or ACS.